Table of Content

- Savings Account Rate Trends

- What Should You Do if the RLLR-based Home Loan Rate of Your Bank is Higher than the Prevailing Market Rate?

- Visualizing the 200-Year History of U.S. Interest Rates

- Historical CD interest rates: 1984-2022

- Monthly Payment

- Do Lenders Give You the Interest Rate Conversion Facility on a Home Loan?

She has more than 30 years’ experience as a writer and editor for newspapers, magazines and online publications. They needed to decrease the desire and/or ability of consumers to buy a home. Take control of your financial future with information and inspiration on starting a business or side hustle, earning passive income, and investing for independence. Each week, you'll get a crash course on the biggest issues to make your next financial decision the right one.

Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication. Consider options from as many mortgage lenders as possible to find the best deal for you. Prospective buyers have saved more than $1,500 over a loan’s term by getting two quotes from lenders, and saved roughly $3,000 when they sought five quotes, according to Freddie Mac.

Savings Account Rate Trends

When banks can't borrow money from other banks, they borrow from the Federal Reserve — the discount rate is the cost for financial institutions to borrow these short-term loans. Federal Reserve Banks set the rate — the higher the rate, the more expensive it is for banks to borrow from the fed. The fed interest rate is a benchmark that banks, credit unions and other financial institutions use to set prices for loans.

The Federal Reserve doesn't have a direct role in setting the prime rate. The target federal funds rate, which is set by the Federal Reserve Board, serves as the basis for the prime rate. When the Fed anticipates future inflation, it raises interest rates slightly to slow it down. Many of the offers appearing on this site are from advertisers from which this website receives compensation for being listed here. This compensation may impact how and where products appear on this site .

What Should You Do if the RLLR-based Home Loan Rate of Your Bank is Higher than the Prevailing Market Rate?

Unless you have a crystal ball that can predict the future, it's impossible to know how much interest rates will rise in the coming five years. Pent-up demand, especially for travel, means inadequate supply to chains still rocked by COVID-19, but Russia's invasion of Ukraine and energy insecurity have raised oil and gas prices. A cash-out refinance is a refinancing option if you have enough equity in your home. With a cash-out refinance, you can tap into home equity you’ve built through repayment of your home loan as well as home value appreciation. You can use that money to pay off other debts or make home renovations.

Although individual credit standing is one of the most important determinants of the favorability of the interest rates borrowers receive, there are other considerations they can take note of. While the best mortgage rate is really the lowest one you can get, you're able to have greater context as to how low or high your rate ranks when looking at the graph from the St. Louis Federal Reserve. In June 1993, rates started to look normal again, with the average one-year CD yield sinking to 3.1 percent APY, Bankrate survey data shows. Here’s a look at the historical ups and downs of CD rates and some background on rate fluctuations through the decades.

Visualizing the 200-Year History of U.S. Interest Rates

These offers do not represent all available deposit, investment, loan or credit products. When the unemployment rate is high, consumers spend less money, and economic growth slows. However, when the unemployment rate is too low, it may lead to rampant inflation, a fast wage increase, and a high cost of doing business. As a result, interest rates and unemployment rates are normally inversely related; that is, when unemployment is high, interest rates are artificially lowered, usually in order to spur consumer spending.

The content created by our editorial staff is objective, factual, and not influenced by our advertisers. If youve recently entered the housing market, youve probably developed a sudden passion for interest rates. This may be particularly true for mortgage loan rates, a topic youve probably given little thought to in the past. If interest rate cost is an important factor for you, you might also consider an adjustable-rate mortgage . The most popular ARM is called the 5/1 ARM, which has a fixed rate for the first five years of the loan and then switches to an adjustable rate for the remainder of the 30-year loan term.

The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. In a period of rising or volatile interest rates—like the current one—it may be wise to lock in a rate that seems affordable for you. Mortgage rates have surged since the start of 2022, which reflects investors’ views that the economy is too hot and that the Federal Reserve will take any necessary steps to cool it down and rein in inflation. The average cost of a 15-year, fixed-rate mortgage has also surged to 6.00%, compared to 2.43% in early January. Before you start shopping around for a lender, you can find out how much you could save by using a mortgage refinancing calculator. Rates for home loans are caught in a tug-of-war between high inflation and the Federal Reserve’s actions to restrain inflation, which have indirectly pushed rates higher.

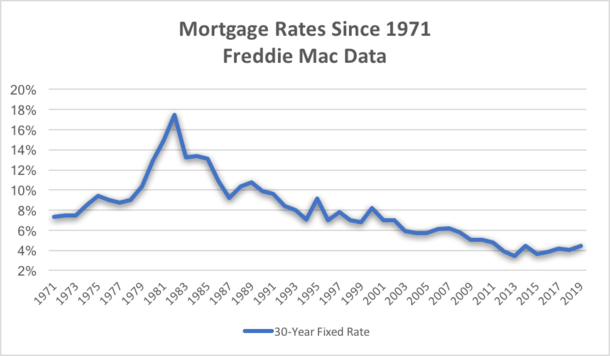

As near-zero rates seem more likely for the extended future, market distortions—such as ultra-low income yields—may become more commonplace. In turn, investors may want to rethink traditional asset allocations between fixed income, equities, and alternatives. After falling for three decades at the turn of the century, interest rates stood at 4% in 1835. That year, president Andrew Jackson paid off the U.S. national debt for the first and only time in history, as debt was seen as a “moral failing” or “black magic” in his eyes. Prior to today’s historically low levels, interest rates fell to 1.7% during World War II as the U.S. government injected billions into the economy to help finance the war.

The Organization of the Petroleum Exporting Countries instituted the embargo. One of the effects of this was hyperinflation, which meant that the price of goods and services rose extremely fast. Were transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money.

With mortgage rates increasing, it might make less financial sense to try to refinance to a lower rate. Generally, it’s best to refinance if you can shave off one-half to three-quarters of a percentage point from your current interest rate, and if you plan to stay in your home for a longer period of time. If you plan to sell your home soon, the cost to refinance might not be worth it. The 1990s saw a dramatic shift in the 30-year rate’s movement, as it plunged to an average of 6.91 percent in 1998, according to Bankrate data.

You’ll also want to consider how long you plan on staying in your home as the closing costs can eat up your savings if you sell shortly after refinancing. The closing costs to refinance run between 2% to 5% of the loan amount, depending on the lender. So you should plan on keeping your home long enough to cover those costs and realize the savings from refinancing at a lower rate.

Valerie Smith is a writer based in Southern California, specializing in legal, real estate, finance, and aviation topics. Valerie is a commercial pilot, FAA licensed aircraft dispatcher, FAA licensed Advanced and Instrument Ground Instructor, California real estate broker, and certified paralegal. Her work has appeared in numerous publications in print and online. A life-long California resident, Valerie holds a Bachelor of Arts degree from San Diego State University and attended Sheffield School of Aeronautics.

Personal loan rates have fluctuated since the early 1970s, but have ultimately decreased over the last four decades. For 24-month personal loans issued by commercial banks, rates are 10.05 percent as of February 2017, according to the Board of Governors of the Federal Reserve System. This is down from 12.38 a decade earlier in 2007, and more than 6 percent lower than the peak rate of 18.65 percent in 1982.

A survey from Fannie Mae showed that only 16% of people think this is a good time to buy a home, a record low. The central bank said it anticipates multiple similar hikes throughout 2022 and 2023 until inflation gets under control. However, opportunities to lock in a lower interest rate do still exist for home buyers and refinancing homeowners. Rate quotes can also vary massively based on the details of your specific scenario. As such, the best use of any timely, accurate rate index is to observe the day-to-day change. A discount point can lower interest rates by about 0.25% in exchange for upfront cash.

No comments:

Post a Comment